Orient Overseas (International) Limited (“OOIL”)

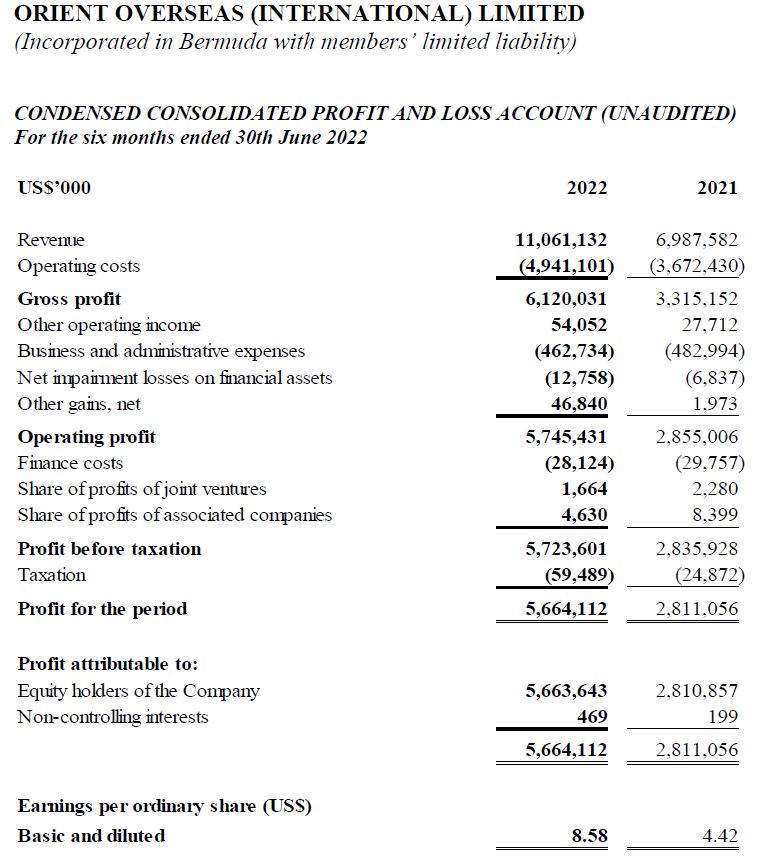

today announced a profit attributable to equity holders of US$5,663.6

million for the six-month period ended 30th June 2022, compared to a

profit of US$2,810.9 million for the same period in 2021.

Earnings per ordinary share for the first half of 2022

was US$8.58, whereas earnings per ordinary share for the first half of

2021 was US$4.42.

The Board of Directors is pleased to announce that the

dividend for the first half of 2022 is approximately 70% of the profit

attributable to equity holders at approximately US$3,962 million, with

an interim dividend of US$3.43 per ordinary share and a special dividend

of US$2.57 per ordinary share.

The outstanding performance of the Group was driven by

the continuing extraordinary conditions prevailing in the container

shipping market. As has been the case for over two years, our market is

neither enjoying an extraordinary demand boom, nor suffering from any

lack of vessels in deployment. Rather, levels of demand, which are

better than expected but not phenomenally strong, continue to outpace

the effective level of supply, which is under significant downward

pressure from a combination of congestion, delays and disruptions.

Understanding this is key to any analysis of the current market

situation and of the outlook.

These market forces pushed freight rates upwards on

most tradelanes, and it is these market forces, in addition to our usual

careful attention to cost control, that have driven the strong

profitability that has been achieved during the period.

Throughout this period, it has been more important than

ever to work closely with our customers. In times of congestion and

disrupted schedules, communication and co-operation help not only to

mitigate the challenges of the current operational situation, but also

serve to consolidate and deepen relationships. We are proud of our

reputation for excellent customer service, and we believe that our

efforts through these turbulent times will stand us in good stead as we

seek to extend collaboration with our customers.

The first six months of 2022 produced the highest

half-year revenue in the Group’s history. Compared to the same period

in 2021, OOCL’s total liner liftings for the first half of 2022 reduced

by 7%, total revenue increased by 61%, and revenue per TEU increased by

74%.

The average price of bunker recorded by OOCL in the

first half of 2022 was US$729 per ton compared to US$449 per ton for the

corresponding period in 2021. The price increase of 62% in the first

half of 2022 has led to a 46% increase in total bunker costs for the

first half of 2022, as compared to the corresponding period in 2021,

even though consumption of both fuel oil and diesel oil were lower in

the first half of 2022 than in the corresponding period in 2021.

The Dual Brand strategy of the Group continues to bring

us many advantages. During these challenging times, it has allowed us

to access additional capacity to offer our customers, and to ensure that

we minimise the risk of equipment shortages. One huge advantage of our

Dual Brand strategy is that it allows us to continue to co-operate in

this way, and to achieve tremendous savings through joint procurement

and efficiencies of scale, without ever impairing our ability to provide

complementary offerings to the market under the banner of each brand.

In the first half of 2022, no new-build container

vessel was delivered, and no new order was placed by the Group. The

twelve 23,000 TEU container vessels ordered by the Group in year 2020

are expected to be delivered starting from 2023, and the ten 16,000 TEU

container vessels ordered last year will be delivered from 2024 fourth

quarter to 2025 fourth quarter.

For the first half of 2022, OOCL Logistics revenue and

contribution had good steady increment as compared with the same period

last year. The revenue of the International Business Units exhibited

healthy growth due to the growing demand of international logistics

services. While Domestic Logistics continued to face fierce

competition, the business unit still managed to maintain stable

revenue. With the effort on streamlining processes and the use of IT

systems, costs were further driven down and resulted in satisfying

improvement in profitability.

Looking forward, we see an array of conflicting signals

that provide little clarity in terms of outlook. Undoubtedly, there

are legitimate concerns about the impact of inflation and interest rate

rises on consumer spending in many key economies. Even if US retail

Inventory-to-Sales ratios remain low, we note some year-on-year

increases in absolute levels of US inventory. Indeed, some larger US

retailers have specifically reported that they are holding higher levels

of inventory.

Yet at the same time, consumers are still purchasing

new goods, even if not necessarily the same goods they were buying last

year, and thus far there has not been a complete return of pre-pandemic

patterns of spending on services as opposed to goods. Furthermore,

forecasts from various port and retail sources in the US suggest ongoing

resilience in the demand for imported goods.

At the time of writing, our ships are sailing full on

our main long-haul tradelanes, and are forecast to continue to be fully

loaded in the coming weeks. There has not been much evidence, so far,

of the kind of significant seasonal uptick that is often a feature of

the traditional Trans-Pacific peak season. We continue to monitor the

situation closely.

Anyone trying to forecast the future of container

shipping must focus on what has created the current market, being the

relationship between supply and demand as mentioned above, and not on

any one individual factor. A proper understanding of the current market

and its outlook must calmly consider each of the wide range of causes

that have created current market conditions.

OOIL, as part of the COSCO SHIPPING Group, continues to

be in the vanguard of the advancement of the container shipping

industry, and will work to provide ever more reliable and resilient

services to our customers. Not only in terms of optimising our network

and intelligent growth of our fleet, but also in terms of broader

integrated supply chain “end-to-end” capabilities and our positioning

among the leaders of the digitalisation of our industry, through IQAX,

GSBN and FreightSmart. This commitment to investing in the future,

along with our focus on ESG, and closer cooperation with our customers,

will position us well to continue to be a Vital Link to World Trade.

As at 30th June 2022, the Group had total liquid assets

of US$11,076.9 million compared with debt obligations of US$805.7

million repayable within one year. The Group remained at net cash

position with a net cash to equity ratio of 0.65 : 1 as at 30th June

2022. The Group from time to time prepares and updates cashflow

forecasts for project development requirements, as well as working

capital needs, from time to time with the objective of maintaining a

proper balance between a conservative liquidity level and an effective

investment of surplus funds.

OOIL owns one of the world’s largest international

integrated container transport businesses which trades under the name

“OOCL”. With around 420 offices in about 90 countries/regions, the

Group is one of Hong Kong’s most international businesses. OOIL is

listed on The Stock Exchange of Hong Kong Limited.

* * *

Issued by: Orient Overseas (International) Limited

For further information contact

Martin Kan Investor Relations (852) 2833 3143

Internet address:

https://www.ooilgroup.com